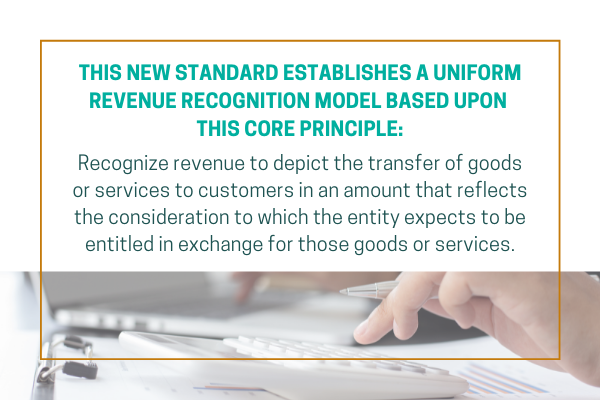

The five-step approach to revenue recognition introduced with Accounting Standards Update 2014-09, Revenue from Contracts with Customers (ASC 606) has gone into effect and significantly changes some financial statements and the recognition of revenue. This broad standard requires management to make judgments and estimates that were not required in the past. It also removed virtually all historical revenue recognition guidelines, including industry-specific requirements. The new revenue recognition framework may impact not only a company’s accounting, but financial reporting, systems, processes, internal controls, financial ratios, and contract language.

ASC 606 changes the way we calculate revenue and the terminology used on the balance sheet. Contract liabilities and contact assets replace many terms, including deferred revenue, costs in excess of billings, and billings in excess of costs. Revenue, however, is not the only account affected by this standard. Commissions and advertising costs may also be affected either through the timing of expenses or through classification on the income statement, with some items now lowering overall revenue instead of increasing expenses.

3 things companies should do when assessing revenue recognition

- Identify all revenue streams. Create a list of how and why money is coming into the company.

- Identify all types of contracts within those revenue streams. Many companies have a standard contract that is used across all customers, others allow for differences in payment terms, discounts, prices, and concessions. Companies need to accumulate all deviations of contracts to fully understand the effect ASC 606 will have on their financial statements.

- Evaluate the contract through the five-step approach and determine if a change in recognition will occur.

Revenue recognition significantly affects many companies across many industries. Smith Schafer is well versed in the new standard and can help to ensure your company is in compliance with the new rules.

Our experts have created the case studies below to assist in understanding these changes. Below are industry-specific examples of how revenue recognition is treated under ASC 606:

Questions?

Smith Schafer is here to help and we are available to assist in the areas in which financial reporting and disclosures will be impacted by:

- Evaluating the impact of the revenue recognition accounting on financial statements, policies, and financial disclosures

- Reviewing contracts to understand how each revenue stream is recognized

- Providing practical recommendations for changes, implementation, and transition considerations

- Consulting with management to determine an approach, if any changes are required to accounting policies and procedures

- Identifying the tax implications of revenue changes